- comparetaxorg@gmail.com

- Link Street 1, Azad Market, Risali, Bhilai (Chhattisgarh)

Blogs Details

2025-11-08 16:22:19

Appeal Procedures under the Income Tax Act, 1961 — Complete Guide

🧾 Appeal Procedures under the Income Tax Act, 1961 — Complete Guide

Taxpayers often face situations where they disagree with the assessment or order passed by the Income Tax Department. In such cases, the Income Tax Act, 1961 provides a detailed appeal mechanism to ensure that every taxpayer gets a fair opportunity to present their case.

This article explains various levels of appeal, relevant sections, and how professional assistance can simplify the entire process of filing and managing appeals.

🔹 What Is an Income Tax Appeal?

An appeal is a legal remedy available to taxpayers who are dissatisfied with the decision or order of the assessing officer.

It is a right to challenge the order before a higher authority, ensuring transparency and justice in the taxation process.

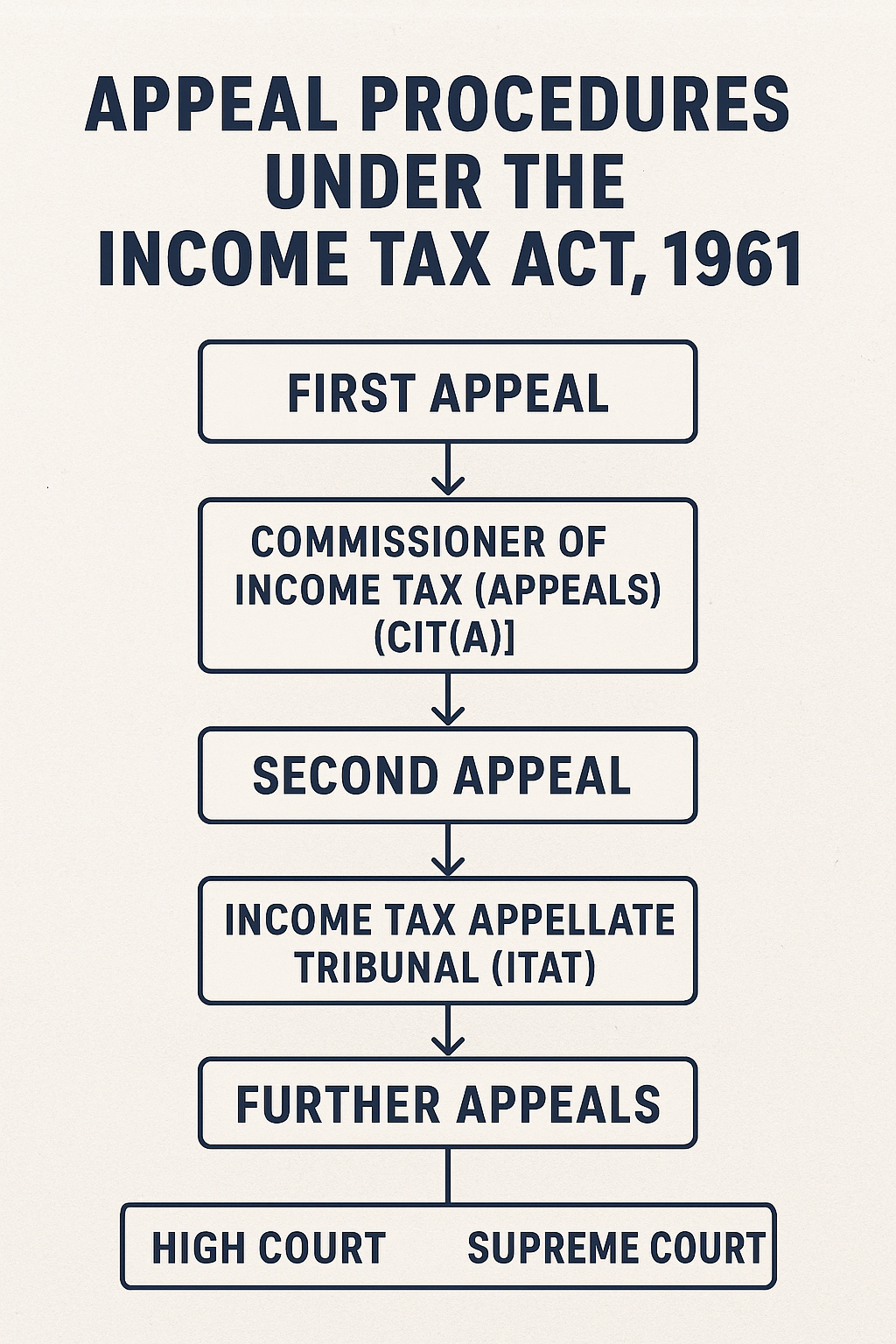

⚖️ 1️⃣ First Appeal – Commissioner of Income Tax (Appeals) [CIT(A)]

Relevant Section: Section 246A to 251

-

A taxpayer can file an appeal before the Commissioner of Income Tax (Appeals) if he/she is aggrieved by an order passed by the Assessing Officer.

-

The appeal must be filed within 30 days from the date of receipt of the order.

-

The appeal is filed in Form No. 35 electronically through the e-filing portal of the Income Tax Department.

CIT(A) has the power to:

-

Confirm, reduce, enhance or annul the assessment.

-

Call for remand reports from the Assessing Officer.

-

Provide reliefs on genuine grounds raised by the assessee.

⚖️ 2️⃣ Second Appeal – Income Tax Appellate Tribunal (ITAT)

Relevant Section: Section 252 to 255

-

If the taxpayer is not satisfied with the decision of the CIT(A), a further appeal can be made before the Income Tax Appellate Tribunal (ITAT).

-

The appeal must be filed within 60 days from the date of the CIT(A) order.

-

The appeal is filed in Form No. 36 and submitted online.

ITAT is an independent judicial body and is the final fact-finding authority.

It can:

-

Admit additional evidence,

-

Pass speaking orders,

-

And even restore cases to lower authorities for fresh consideration.

⚖️ 3️⃣ Further Appeals – High Court and Supreme Court

(a) Appeal to High Court – Section 260A

-

Can be filed against an order of ITAT on substantial questions of law.

-

Time limit: 120 days from receipt of ITAT order.

(b) Appeal to Supreme Court – Section 261

-

Lies against the judgment of the High Court.

-

The Supreme Court’s decision is final and binding.

📑 4️⃣ Revision by Commissioner – Sections 263 and 264

Apart from the appeal mechanism, the Act also provides for revisionary powers of the Commissioner of Income Tax:

-

Section 263: If the order passed by the Assessing Officer is erroneous and prejudicial to the interest of revenue, the Commissioner may revise the order.

-

Section 264: The assessee may apply for revision to the Commissioner if he feels that the order is not just or proper.

💻 5️⃣ How We Help in Filing Income Tax Appeals

Filing an appeal requires a perfect blend of technical knowledge and practical expertise.

We assist our clients throughout the process with a professional approach:

-

Detailed Review:

We thoroughly review the assessment order, supporting documents, and grounds of disallowance. -

Drafting Grounds of Appeal:

We prepare well-structured and legally sound grounds ensuring all relevant facts and laws are covered. -

Preparation & Filing:

We prepare Form 35 / Form 36 with supporting statements and file them online as per current e-filing procedures. -

Representation before Authorities:

We represent our clients during hearings before CIT(A), ITAT, and higher appellate forums with full documentation and arguments. -

Post-Appeal Compliance:

Once the order is received, we guide on effect-giving procedures, rectification, and refund claims if any.

📘 Example – Common Situations for Filing Appeal

-

Addition under Section 68 (Unexplained Cash Credit)

-

Disallowance of Business Expenses under Section 37

-

Penalty Orders under Section 271(1)(c)

-

Reassessment Orders under Section 147/148

-

Denial of Deduction under Section 80 Series

✅ Conclusion

The appeal process under the Income Tax Act, 1961 is an essential part of the taxpayer’s right to justice. However, filing an appeal requires expertise, timely action, and precise drafting.

With our experienced audit and tax team, we ensure that your appeal is handled professionally — from drafting grounds to representing before appellate authorities — helping you achieve a fair and favorable resolution.

.png)